Innovation accounting enables startups to prove objectively that they are learning how to grow a sustainable business. Innovation accounting begins by turning the leap-of-faith assumptions into a financial model.

Vanity metrics are cumulative totals and gross numbers such as total revenue and total number of customers. These can be misleading and do not show trends that can be attached on because they hide confounding data. For a report to be considered actionable, it must demonstrate clear cause and effect. Otherwise, it is a vanity metric. With vanity metrics, it’s so common to have a meeting in which the marketing departments thinks the numbers went up because of a new PR or marketing effort and the engineering department thinks the better numbers are the result of the new features it added.

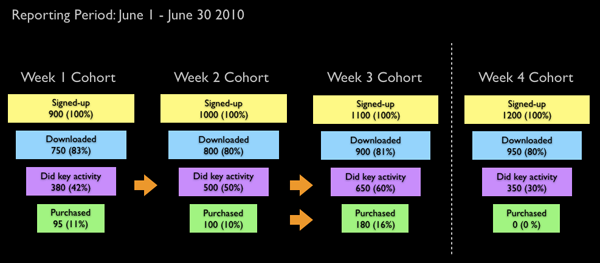

Cohort analysis is one of the most important tools of startup analytics. Actionable metrics like a cohort analysis look at the performance of each group of customers that comes into contact with the product independently. Each group is called a cohort. The graph can show the conversion rates of new customers who joined your company in each indicated month. Each conversion rate shows the percentage of customer who registered in that month who subsequently went on to take the indicated action.

Here are examples of a cohort graph

A split-test experiment is one in which different versions of a product are offered to customers at the same time. By observing the changes in behavior between the two groups, it is easier to make inferences about the impact of the different variations.

Only 5 PERCENT of entrepreneurship is the big idea, the business model, the whiteboard strategizing, and the splitting up of the equity.

The other 95 percent is the hard work that is measured by innovation accounting: product prioritization decisions, deciding which customers to target or listen to, and having the courage to subject a vision to constant testing and feedback.

No comments:

Post a Comment